Okay so I am going to be really honest with you right now.

When I left my 9-5 after 13 years and started running my own creator business, I had absolutely no idea what a business bank account even was.

Like I knew it existed the same way I knew RRSPs existed.

Something adults with their lives together had.

Not something I had ever actually needed to think about because for 13 years a company handled all of that for me.

My salary showed up every two weeks. My taxes got deducted automatically. I never once had to think about any of it.

And then I went self employed and suddenly I was googling things like “do I need a business bank account if I am a self employed creator in Canada” at 11pm with a cup of tea and a mild sense of panic.

If that sounds like you right now, you are in exactly the right place.

Because I have been through the confusion of figuring all of this out with genuinely zero finance background and I am going to share what I now know in the most human way possible.

- Do I Actually Need A Business Account?

- What I Wish Someone Had Told Me to Look For

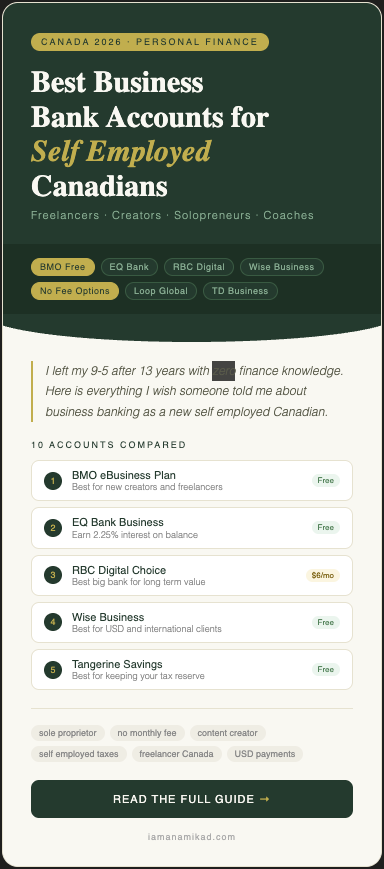

- The Accounts Worth Actually Looking At

- 1. BMO eBusiness Plan

- 2. EQ Bank Business Account

- 3. RBC Digital Choice Business Account

- 4. TD Basic Business Plan

- 5. Scotiabank Right Size Account for Business

- 6. CIBC Smart Account for Business

- 7. Tangerine Business Savings Account

- 8. Wise Business Account

- 9. Loop Global Banking

- 10. Meridian Credit Union Business Account

- My Honest Recommendation After Going Through All of This

Do I Actually Need A Business Account?

This was my first question too and my honest first reaction was to just keep using my personal account. I mean money is money right. It all goes into the same place anyway.

Wrong. And I found out the hard way.

My first tax season as a self employed person I sat down with my accountant and she asked me to go through my bank statements and highlight every business transaction.

I was using my personal account. So there I was, squinting at twelve months of transactions trying to remember whether that $47 Tim Hortons charge was a client meeting or just a regular Tuesday.

Whether that Amazon order was for my home studio setup or for my kitchen.

It took hours. My accountant charged me extra for the time it took to sort through the chaos.

And I still probably missed legitimate deductions because I genuinely could not remember.

A dedicated business account fixes all of that. Your business money goes in. Your business expenses come out.

Everything is clean and separate and your accountant does not look at you with that particular kind of quiet disappointment.

There is also the professional angle.

I started sending invoices with my personal banking information on them and one of my first brand clients actually asked me to confirm it was a legitimate account before processing payment.

That was a humbling moment. A business account just looks like you know what you are doing even when you are still figuring it out.

What I Wish Someone Had Told Me to Look For

I had no framework for comparing bank accounts because I had never had to think about this before.

At my 9-5 the company had everything set up already.

So when I started looking at options I was genuinely overwhelmed.

Here is what I eventually figured out actually matters for a creator running their own business.

Monthly fees.

Some accounts charge you just for existing which felt offensive to me as someone in the early stages of building income.

Zero fee options exist and they are perfectly legitimate.

Some accounts give you a set number of transactions per month and then charge you for each one after that.

As a creator you are probably receiving payments from brands and UGC clients, paying for software subscriptions, sending money to contractors and doing a lot of small transactions.

This adds up fast.

Whether it connects to your bookkeeping software.

I use Wave which is free and it connects directly to some bank accounts so my transactions import automatically.

This saves me an embarrassing amount of time every month.

Whether you can open it online.

I did not want to go sit in a bank branch with a stack of documents.

Some accounts you can open from your phone in ten minutes. Others require a branch visit.

As someone who is now her own boss and has back to back content days, the online option matters.

The Accounts Worth Actually Looking At

1. BMO eBusiness Plan

Monthly fee: Nothing. Zero. Free.

Best if: You are just getting started and receive money digitally

This was the first account I looked at seriously and honestly it made me feel a lot better about the whole situation.

The BMO eBusiness Plan is the only genuinely free business account from one of Canada’s major banks.

You get unlimited electronic transactions which means all the Interac e-Transfers, bill payments and online transfers you want with no per-transaction charges.

And sole proprietors, which is what most of us are when we first go self employed, can open it entirely online without going anywhere near a branch.

The one thing that caught me off guard when I was researching this is that they charge for cash deposits. $2.25 per $1,000.

For me personally this is not an issue because every client pays me by e-Transfer or direct deposit.

But if you sell physical products or get paid in cash at any point, factor that in.

For a brand new content creator running a digital business, this is genuinely a great starting point.

2. EQ Bank Business Account

Monthly fee: Also free

Best if: You tend to keep a decent amount of money sitting in your account between payments

I did not know this was a thing until I started digging into options and it kind of blew my mind.

EQ Bank actually pays you interest on the money sitting in your business account.

Like you just have money there, doing nothing, and it earns 2.25% interest on the full balance with no catches and no minimum amount required.

At my old 9-5 I was just letting my paycheck sit in a regular chequing account earning basically nothing.

The idea that my business account could earn money just by existing in it is still something I find genuinely exciting as a financial late bloomer.

EQ Bank is a real Canadian bank with proper CDIC deposit insurance the same as the big banks, so your money is protected the same way.

The honest limitations: it is completely online, there is no branch, you cannot deposit cash and it does not support USD.

And if you are in Quebec it is not available there.

But for a creator who gets paid digitally and works with Canadian clients, none of that is likely to be a problem.

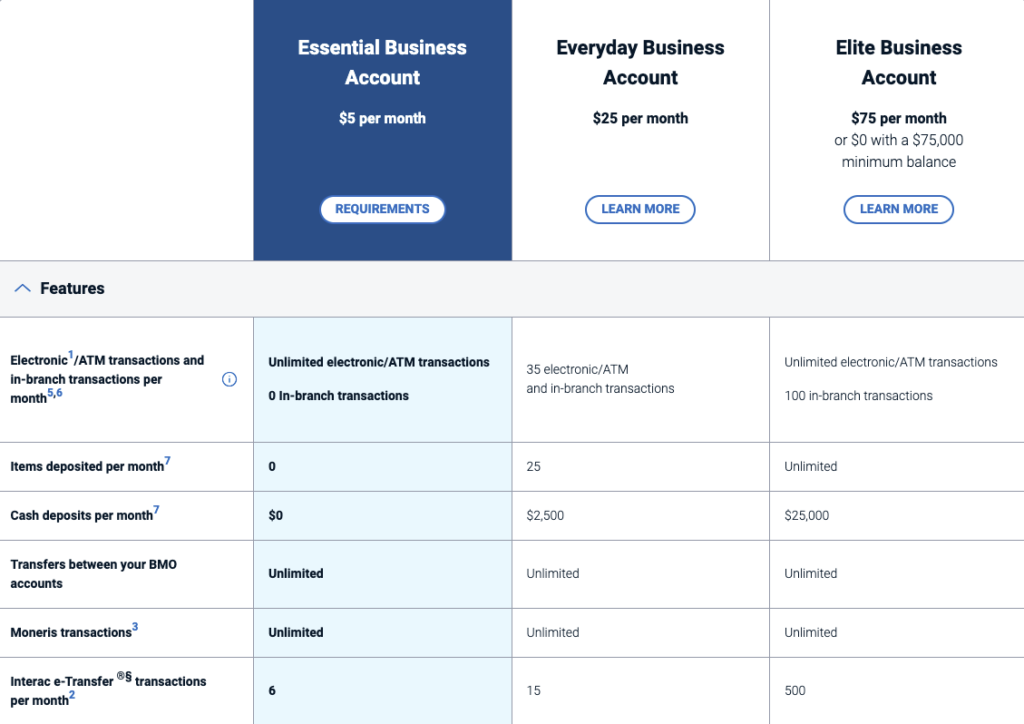

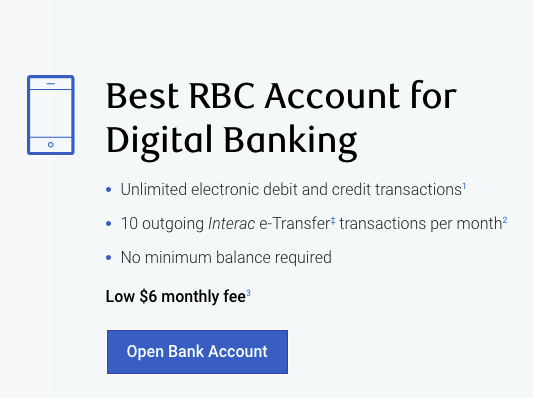

3. RBC Digital Choice Business Account

Monthly fee: $6 a month

Best if: You want the security of a big recognizable bank without paying a fortune

I have to be real.

When I first left my job I really wanted to feel legitimate.

Like I wanted a proper grown up business bank account from a proper bank with a name I recognized.

And RBC Digital Choice is about as close to that as you can get for $6 a month.

You get 12 free transactions per month which honestly covers most creator businesses that are in the early growth stage.

The app is really good and it connects to accounting software without drama.

But here is the bigger reason I keep seeing this account recommended for self employed Canadians.

If down the road you want to apply for any kind of financing, a business loan, a line of credit or even a mortgage as a self employed person, having an established banking history with a major bank like RBC works in your favour.

They can see your transaction history, your income patterns and your business health over time.

That long term relationship has value that is hard to put a number on right now but becomes very real later.

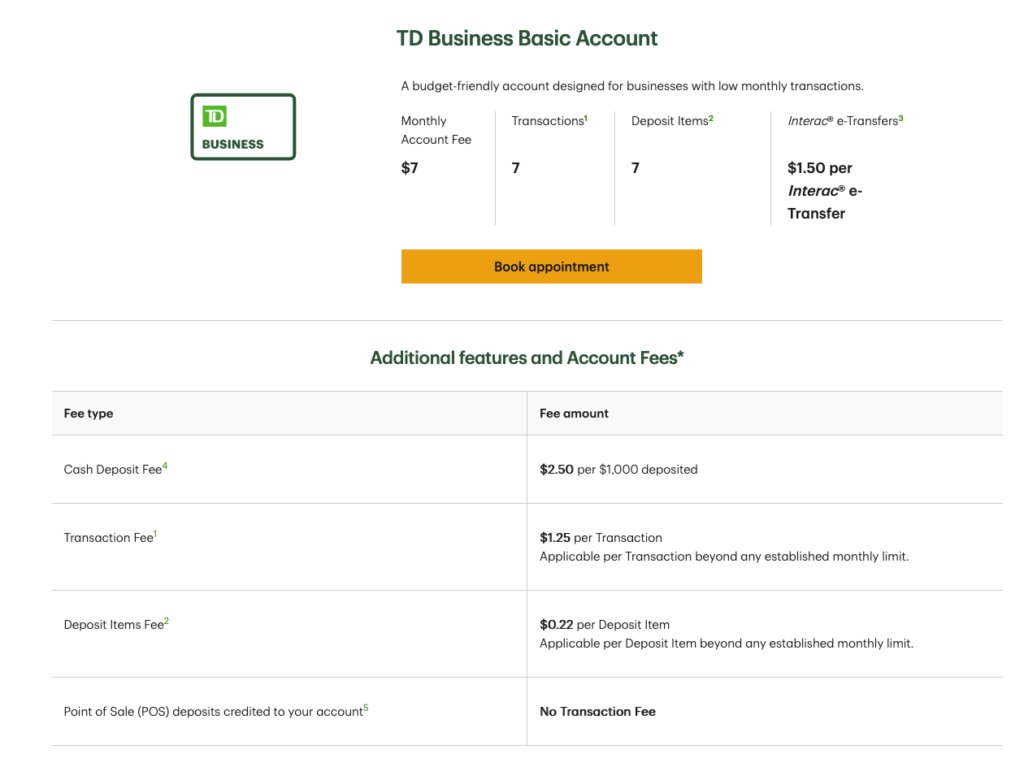

4. TD Basic Business Plan

Monthly fee: $5 to $19 depending on which plan

Best if: You might occasionally need to actually walk into a bank

TD was the bank I had my personal account with for most of my adult life so there was a comfort factor in looking at their business options when I first went self employed.

That familiarity is worth something when you are already dealing with a hundred new things at once.

Their business account plans start at a very manageable monthly fee and they have branches and ATMs basically everywhere in Canada which matters on those rare occasions when you need to do something in person.

The digital banking is solid and the app is one of the better ones for day to day use.

TD also runs welcome offers for new business account holders reasonably regularly so it is worth checking their current promotions directly because you might get cash back just for opening the account and setting up a direct deposit.

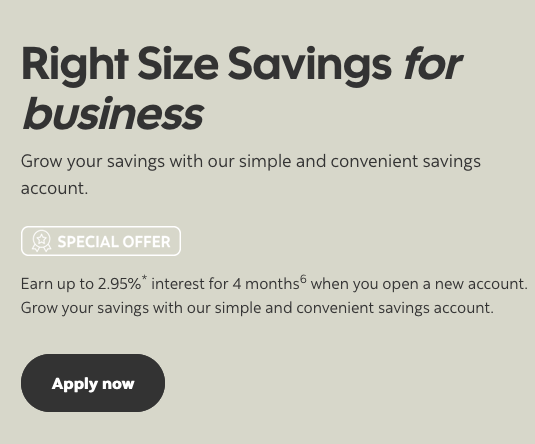

5. Scotiabank Right Size Account for Business

Monthly fee: $6.95 to $21.95

Best if: You think you might eventually work with international clients

I will be honest, I did not look at Scotiabank very seriously at first because I associated them more with my parents’ banking than with my new creator business life.

But a few creator friends in bigger markets mentioned they use Scotia specifically because of how easy it is to deal with international payments once you start working with US brands.

The entry level account is reasonable and Scotia has a product called the Professional Plan Plus that a lot of consultants, coaches and service providers use.

If your creator business eventually moves into coaching or consulting, that specific account might be worth a look.

6. CIBC Smart Account for Business

Monthly fee: $20 to $25

Best if: You sometimes receive physical payments or deal with cheques

CIBC is on the pricier end for a self employed creator just starting out and I would probably not recommend it as a first account unless you specifically need the cash and cheque deposit capability that comes included.

That said, once you are generating more consistent income and want access to a full suite of business financial products from a major bank, having a CIBC relationship has its benefits.

Every big bank has slightly different lending criteria and products and being an existing customer always makes that process smoother.

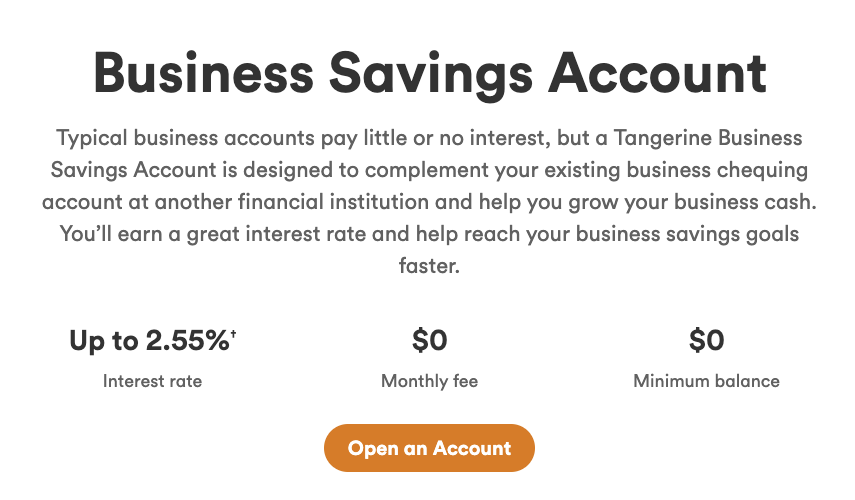

7. Tangerine Business Savings Account

Monthly fee: Free

Best if: You need somewhere to stash your tax money away from your spending account

Okay this one is not technically a chequing account but I am including it because it solved one of the most stressful parts of my first year as a self employed person.

Nobody told me I had to save for my own taxes.

At my 9-5 it just happened automatically.

My first year running my own business I spent money as it came in because it felt like income without really processing that the CRA was going to want a significant portion of it back.

The rule I now follow religiously: every single time a payment hits my account I immediately transfer 25 to 30% of it into a completely separate savings account that I do not touch.

Tangerine’s business savings account is free, earns decent interest and because it is a bit removed from my main account I am less tempted to dip into it.

This single habit is the difference between a normal tax season and a panic spiral in March.

Set it up alongside your main chequing account from day one.

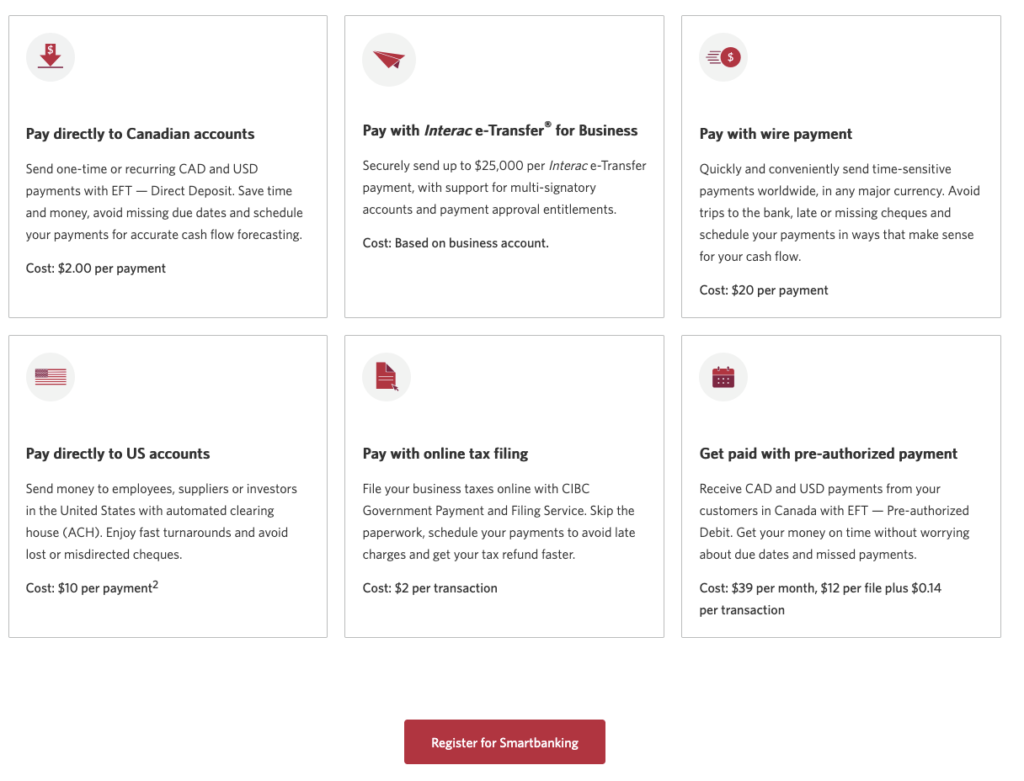

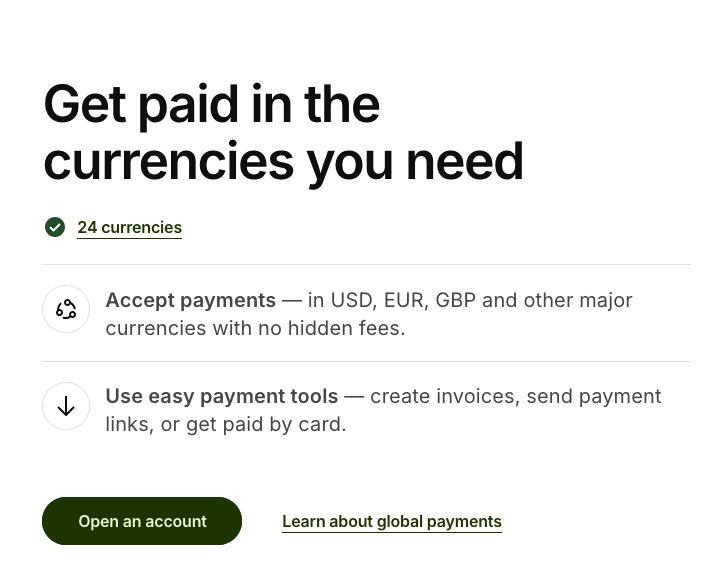

8. Wise Business Account

Monthly fee: Free to open, small fees per transfer

Best if: You work with brands or clients outside Canada

This is what I use right now.

Wise Business changed how I handle getting paid by US brands for UGC and creator work.

Here is the thing. When you receive USD into a regular Canadian bank account, the bank converts it to CAD using their own exchange rate which is often 2.5% to 3% worse than the actual mid-market rate.

On a $500 USD payment that might not sound like much.

But when you are doing regular brand deals and getting paid in USD it adds up to real money over the course of a year.

Wise gives you a real US bank account number.

So when a US brand pays you it goes in as USD at the mid-market exchange rate with a small transparent fee, not the hidden markup that traditional banks quietly take.

You then convert it when you choose at a rate that actually makes sense.

It is not a replacement for your main Canadian business account because it does not do Interac or Canadian bill payments.

But as a companion account for anyone doing work with international clients it is one of the most genuinely useful financial tools I have found since going self employed.

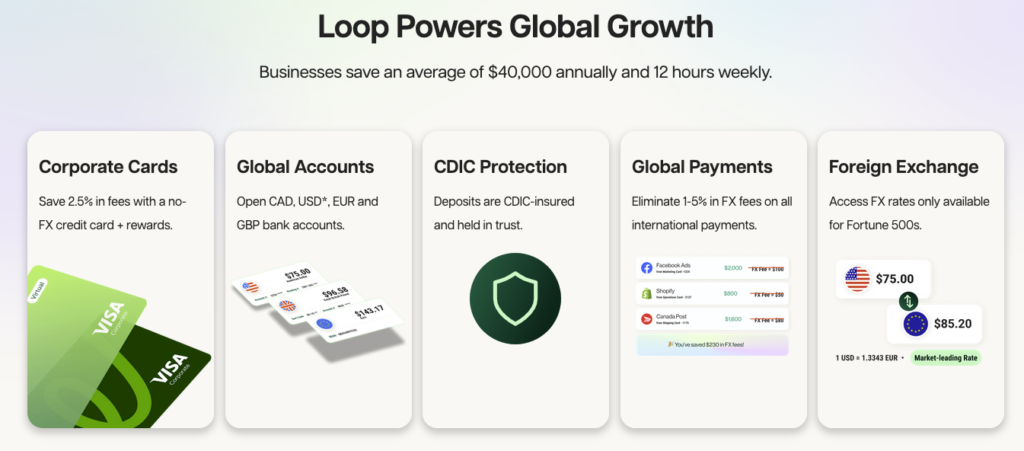

9. Loop Global Banking

Monthly fee: Free on the base plan

Best if: You are regularly dealing with multiple currencies across different client markets

Loop is newer and a lot of creators I know had not heard of it until recently.

The pitch is simple: one account that handles CAD, USD, GBP and EUR without charging you conversion fees when you move between them.

For a creator whose business is growing into different markets and who is juggling payments from clients in different countries, Loop reduces a lot of the headache and cost of moving money internationally.

The free plan covers most of what an individual creator business needs.

10. Meridian Credit Union Business Account

Monthly fee: Less than a dollar a month

Best if: You are based in Ontario and like the idea of a community banking relationship

I grew up thinking credit unions were just for people who did not qualify for big bank accounts which was completely wrong and slightly embarrassing to admit.

Meridian is a federally regulated financial institution and their business account costs basically nothing per month.

You get unlimited free transfers and deposits and the transaction fees are waivable if you keep a minimal balance.

For an Ontario based creator running a lean business and watching every dollar in the early stages, Meridian is an overlooked option that is genuinely worth considering.

The only catch is that the physical branches are Ontario only so if you are elsewhere in Canada and need in person banking this one will not work for you.

My Honest Recommendation After Going Through All of This

If you are a Canadian content creator or online business owner who is new to all of this and just wants to do the right thing without overthinking it, here is the simple version.

Open the BMO eBusiness Plan or EQ Bank as your main account if you want zero fees.

If you work with brands or clients in the US, also open a Wise account. It will save you money almost immediately.

Open a completely separate savings account, Tangerine works great for this, and put 25 to 30% of every payment you receive into it for taxes. Never skip this step.

That is genuinely all you need to start.

You can optimize and switch things around as your business grows.

But getting clean separation between your personal and business money from day one is the single most important thing you can do for your financial sanity as a new self employed Canadian.

Thirteen years of someone else handling this stuff meant I had to figure it all out at once when I finally went out on my own.

I am hoping this saves you at least some of that confusion.

Everything in this post reflects my personal experience and research as a self employed Canadian. Account fees, interest rates and features change regularly so always check directly with the bank or financial institution before you open anything.